To achieve superior growth, a company needs to get its organic growth right, but acquisition strategy is a crucial and very powerful tool. In this article, I delve into my experience as a CFO to provide an insider’s guide to a successful M&A strategy.

By Robbie Taylor, M&A expert and former CFO*

For athletes to perform at their potential, they have to employ a strategy that at least addresses the elements of nutrition and training. Ignoring one of these elements will yield results below potential. Similarly, a high-performance company should employ the dual strategies of organic and acquisitive growth to achieve superior returns in line with its 'genetic' potential: the potential of its industry, geographic location and other factors.

Organic growth

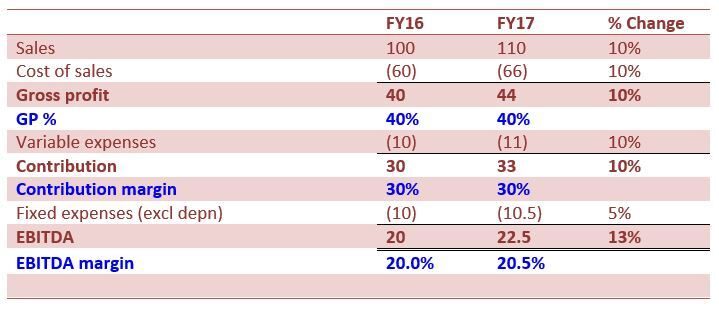

Assuming your company has an existing revenue and margin structure as shown in Table 1 (FY16), and then achieves growth of 10% and experiences inflation of 5%, your FY17 results would be as indicated:

Table 1 - Organic Growth Income statement

Due to the cost control at fixed cost level, the EBITDA margin has actually increased by 13% when sales have only increased by 10%. This is a very simplistic but accurate demonstration of the theory behind superior returns on an organic basis: increase contribution and contain fixed costs.

The practical challenge of increasing contribution organically revolves around increasing sales while keeping the cost of sales and variable expenses constant as a percentage. Increases in sales come from new markets, new products and new geographies.

Example: Complementary and alternative medicines (CAMs) is an industry that has been particularly active in developing new markets and new products. Not long ago, the sports nutrition industry was very basic, with product offerings directed towards the bodybuilding section of the market. Today there are sports nutrition products ranging from instant energy through endurance supplements, to recovery drinks and protein formulae. Almost every sport is catered for in the market and supplementation by lean and light athletes like cyclists, runners and triathletes is more pervasive than protein loading by body builders. This is a good example of very healthy organic growth in a sector.

Clearly there are significant challenges in utilising the organic growth method alone on a long-term basis, the sustainability becomes a challenge as your organisation gains market share to saturation point, and then the variable costs no longer remain a constant percentage as new geographies and cultures are incorporated.

Acquisitive growth

Acquisitive growth is a very effective means of achieving superior returns for the shareholders, provided the acquired businesses are bought at a good price earnings (PE) ratio, and that the acquired company is a good cultural fit. As Warren Buffet said: "Rather buy a good company at a fair price than a fair company at a good price."

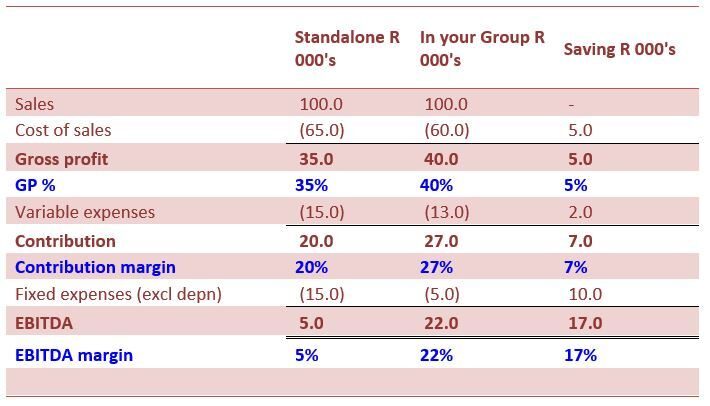

Two income statements of the target

There are two income statements for a target: its existing income statement and the income statement it would have if it were part of your group. This is an incredibly important distinction to understand if one is to affect a successful acquisition strategy and is perhaps one of the most important aspects of the acquisition process.

Targets which may not look appetising on their own can become jewels in your crown if they would benefit from being part of your group.

Assume that, once you acquire the target, it will move production to your facility, resulting in a saving on their cost of sales. At the same time, they will make use of your sales and distribution network, providing further savings, and finally, they will use your accounting, administration, legal and payroll functions saving fixed costs. This is illustrated in an example in Table 2.

Table 2 - A Target's Two Income Statements

In this example, a business with a very modest EBITDA as a standalone company shows incredible results when part of your group. This informs the very crucial second variable in the acquisition process - the price.

In this example, a business with a very modest EBITDA as a standalone company shows incredible results when part of your group. This informs the very crucial second variable in the acquisition process - the price.

In the above example, and assuming you are prepared to pay an EBITDA multiple (PE) of say 8, you'd value the standalone at R40 million, but in reality, you should consider that up to a price of R176 million you would not be overpaying (once again with a lot of assumptions - this is theoretical after all!). Also, the seller may be asking for R50 million, the market value would be slightly less, but knowing what you know about the two income statements you would be able to strongly motivate to your investment committee that a price of R50 million represents a significant price discount for this business, that you would get your money back in just over two years, and that it would result in real value to your shareholders.

Example: The best examples of these kind of companies are 'bolt-ons'. In a previous business, we established 'platform' companies that were the foundation for the division, they typically had a production capability, distribution, marketing, merchandising and new product development. When buying a new company in this division we would look for bolt-ons and buy the business with the expectation that the variable income and expenses (the contribution) would be bolted onto our platform with minimal additional fixed expenses. This is common practice in pharmaceutical companies, where dossiers are bought and sold. Effectively, there is no fixed cost being purchased in these transactions.

Back to organic growth

All the acquisitions you make this year will be part of the existing business from next year and will be subject to the organic growth expectations of the rest of your existing business. Too many companies grow acquisitively using the financial models above, but don't have the operational management to achieve the expected results for the combined group, or to operate the larger entity in an efficient and profitable manner.

Issues such as cultural fit, coordinated marketing efforts, change management, IT systems and other factors too numerous to mention will be working against the successful integration of the new company, and, while none of these are insurmountable, one would be naïve to take this path without a very good plan to address them.

*Robbie Taylor is a CA, has listed two companies on the JSE, has been involved in over 65 acquisitions, and was nominated for the 2015 CFO Awards for his role at Ascendis Health. He now runs Business Transaction Services, a boutique business transaction advisory company providing services to businesses wanting to buy, sell, merge or fund for growth.