Oil-exporting economies like Nigeria and Angola will continue to be hardest hit when it comes to the slowing momentum of GDP growth in Africa. In this first part of RMB's Africa outlook 2016, authors Celeste Fauconnier, Nema Ramkhelawan-Bhana and Neville Mandimika look at the expected real GDP growth in selected economies and the long list of risks to growth.

- Moving into Africa? Register for our CFO event on Wednesday 16 March 2016

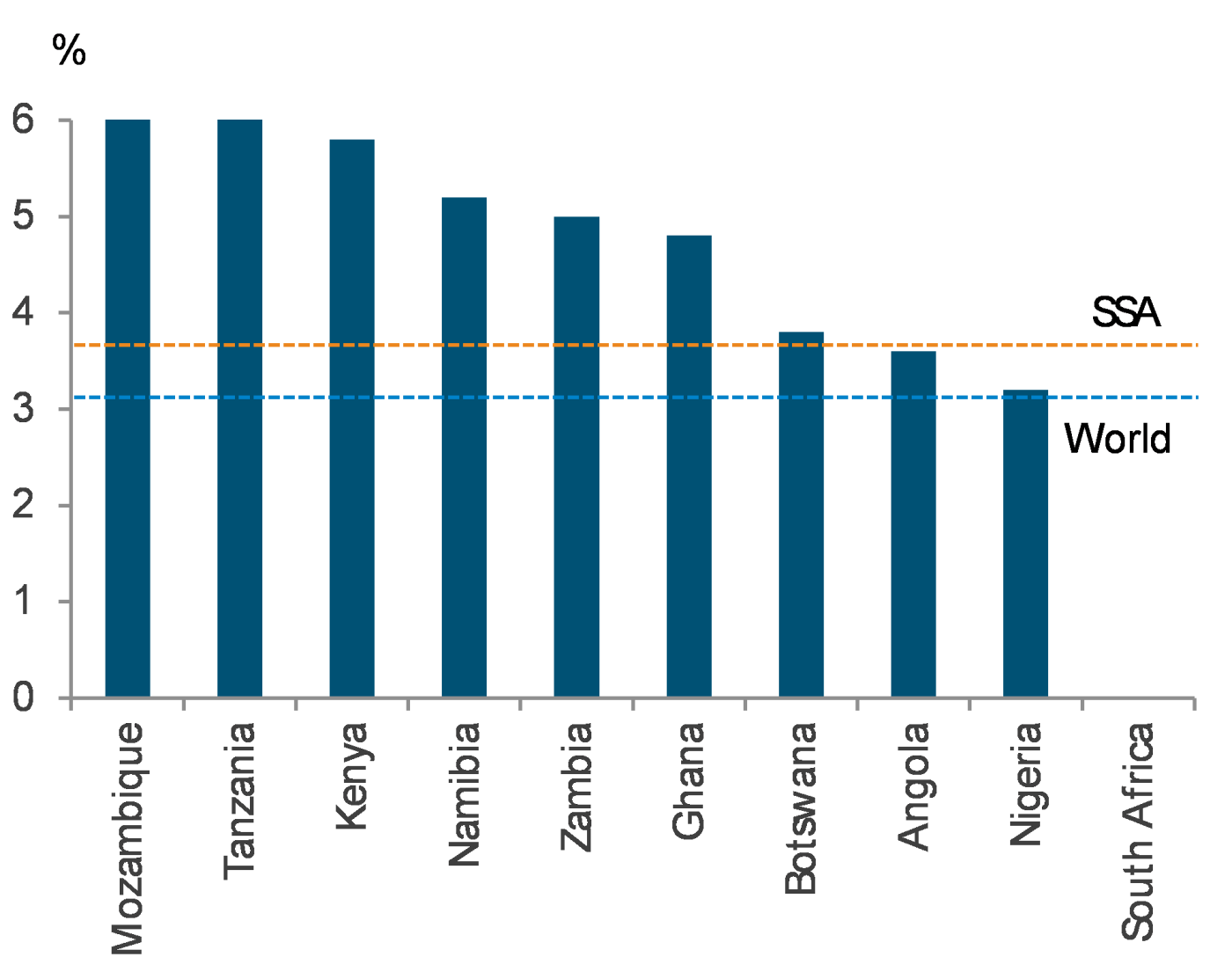

Sub-Saharan Africa (SSA) will continue its economic struggles over the medium term. There has been a sharp deceleration in the region's growth momentum owing to the cyclical downturn in commodities prices and less-supportive financial conditions. The IMF estimates real GDP growth of 3.75% for 2015 and 4.25% for 2016.

This is part 1: Real GDP Growth of RMB's Africa Outlook 2016. Also read part 2: Monetary policy, part 3: Fiscal policy and part 4: Financial markets.

Selected economies

Looking specifically at the resource-rich countries, the oil-exporting economies like Nigeria and Angola were hardest hit in 2015 and the economic pressure will certainly continue in 2016 and 2017 given the deteriorated outlook for the oil price. Both countries will grow below 4% in 2016 from levels of 7% over the past decade.

Mozambique's strong growth over the past five years will now be hampered by lower global coal prices and infrastructure inadequacies, bursting the country's mining boom bubble and causing some firms to cut production and investment. However, we still believe that capital investment into the coal and oil and gas industries will keep growth rates above 6% over the forecast period (Figure 1).

Figure 1: RMB's real GDP growth forecasts for 2016 (Source: RMB Global Markets, data as at January 2016)

Middle income, resource-driven economies like Zambia and Ghana are also facing commodities price problems, especially from a copper and gold sector perspective, which are key foreign exchange earners. Together with the deteriorating fiscal environment and the consolidation as a consequence, growth will remain at the cusp of 5% in 2016.

Botswana and Namibia will face similar challenges as diamond revenues, specifically, are negatively affected by weak global demand, elevated stock levels and tight credit conditions for diamond site holders. But Namibia will experience some respite due to increased uranium production as the Husab mine comes online, while zinc, copper and gold production increases.

The only non-resource-driven economy in our portfolio, Kenya, will in fact receive a boost from the downturn in the commodities price cycle, especially as fuel purchases make up a large chunk of the import bill. Also, Kenya will continue making progress toward establishing itself as a global energy producer. But sudden shocks to the exchange rate, terror threats, further monetary policy tightening and potential fiscal folly ahead of the 2017 presidential elections are key risks to our 6% average growth outlook for 2016 and 2017.

Palpable risks to growth

Unfortunately, the risk list is long and illustrates how sensitive SSA economies remain to internal and external shocks. Investment and economic diversity are key to overcoming some of these hurdles, but in SSA, these solutions are slow in progress. The biggest risks for 2016 and 2017 include fiscal consolidation (with lower social spending as a consequence); low commodity prices; droughts; electricity shortages; lower consumer spending; funding challenges; a further China economic downturn; dollar gains; lower FDI and geopolitical risk.

For queries, contact:

Jacky Buys

Global Markets: Corporate Treasury Solutions

[email protected]

+27 21 4469333

+27 83 3219751

- Stay connected, up to date and in the loop on what is happening in the world of finance and keep track of newly published expert insights and interviews with CFOs and CEOs. Become an online member and receive our newsletter, follow us on Twitter, like us on Facebook and join us on LinkedIn.