In 2016 investors are even more likely to scrutinise the effectiveness of domestic policies, the strength of governance, the sensitivity to commodities price trends and the sustainability of debt burdens. In this fourth part of RMB's Africa outlook 2016, authors Celeste Fauconnier, Nema Ramkhelawan-Bhana and Neville Mandimika look at the financial markets, Eurobonds and currency risk, as financial markets are becoming more skilled at mitigating the unusual risks presented by African currencies.

- Moving into Africa? Register for our CFO event on Wednesday 16 March 2016

Funding less forthcoming

The appetite for local currency assets petered out in 2015 as unprecedented currency weakness eroded investor returns. Regulatory adjustments will prove challenging this year. Authorities are likely to lean against the wind to stabilise financial markets but risk speculative outflows.

This is part 4: Financial markets of RMB's Africa Outlook 2016. Also read part 1: Real GDP Growth, part 2: Monetary policy and part 3: Fiscal policy.

We anticipate a flattening in Kenya and Nigeria's yield curves as investors shorten duration to mitigate further currency weakness. Tighter monetary conditions in both economies imply less money market liquidity and hence higher short-term yields. The longer end of the KES and NGN curves will be informed by the inflation and public debt profiles of each economy.

Numerous local currency bond markets are still in the nascent stage of expansion, owing to various structural constraints. This is evident in Angola and Mozambique, whose governments are exposed to higher repayment and rollover risks due to shallow domestic bond markets with generally low levels of debt capitalisation. Outside of Southern Africa, Nigeria and Kenya provide viable opportunities for investment in a variety of money market and fixed income instruments.

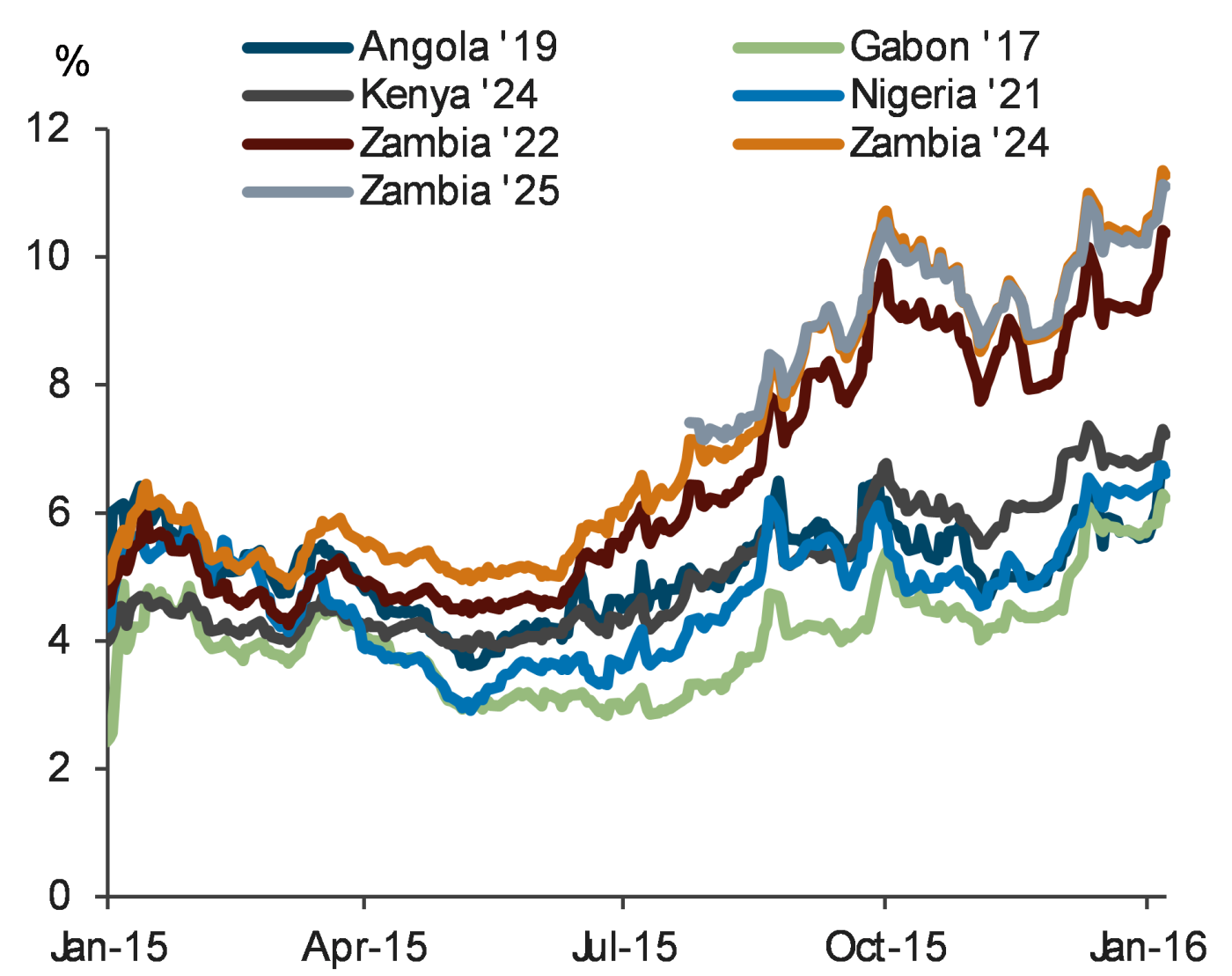

Investors more discriminating of US dollar-denominated debt

The exuberance for Africa's US dollar-denominated debt has dissipated, as evidenced by a continued sell-off in emerging markets. The yield spread between SSA Eurobonds and comparable US Treasuries has widened steadily since May 2015, with the yields on sovereign bonds (outside of Cote d'Ivoire, Rwanda and Seychelles) trading roughly 300bp above their historical averages.

Figure 4: Selected SSA US dollar yield spreads. (Source: Bloomberg, RMB Global Markets, data as at January 2016)

Investors will certainly become more circumspect with regards to African Eurobonds as the competition for global funding intensifies. They are likely to scrutinise the effectiveness of domestic policies, the strength of governance, the sensitivity to commodities price trends and the sustainability of debt burdens. Eurobond positions will only be considered viable when there is adequate liquidity and financing to meet debt servicing obligations without the issuer having to draw down on foreign reserves. This implies prudent fiscal policy management and a narrowing of current account imbalances, which are vital to sustaining market confidence.

In a less severe global environment, elevated yields could possibly entice investors wanting exposure to African economies that are perceived to be more politically and macroeconomically sound.

However, the macroeconomic backdrop has become less conducive to Eurobond issuances on account of domestic constraints and global challenges, not least of which is Fed tightening, resulting in a re-pricing of African credit. The upshot is that rising US Treasury yields will increase the liquidity premium on fresh Eurobond issuances across SSA, exacerbating borrowing costs for new and experienced issuers alike. This is not entirely unwelcomed as it could prevent a build-up of financial imbalances and a reprisal of Africa's debt crisis.

Exchange rates volatility the norm rather than the exception

Subdued commodity prices and concerns over dual deficits are likely to exert depreciatory pressure on various currencies in 2016, particularly those that are directly correlated to resource prices. Exogenous factors will impact the more globally traded currencies like the rand, Kenyan shilling and Mauritian rupee.

The extent to which central banks smooth currency fluctuations will depend on the nature of their influence on domestic foreign exchange markets, via direct intervention and regulation, and the effectiveness of resources at their disposal. Exchange rates will act as an automatic stabiliser to correct fiscal and current account imbalances.

Financial markets are becoming more skilled at mitigating the unusual risks presented by African currencies. Though the extent of financial development may vary, selected African markets offer the necessary derivative instruments to facilitate effective risk management. However, the application of these instruments is dependent on existing exchange controls, which can limit the extent of offshore participation in certain markets.

For queries, contact:

Jacky Buys

Global Markets: Corporate Treasury Solutions

[email protected]

+27 21 4469333

+27 83 3219751

- Stay connected, up to date and in the loop on what is happening in the world of finance and keep track of newly published expert insights and interviews with CFOs and CEOs. Become an online member and receive our newsletter, follow us on Twitter, like us on Facebook and join us on LinkedIn.